Please refer to “Energy Concessions Term” in the Valuation Kit.

Roads

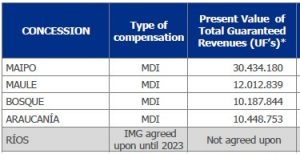

It corresponds to the dates according to the MDI (Mecanismo de Distribución de Ingresos) methodology; These dates are reviewed each year in accordance with the executed and projected toll revenue. The validity of the concessions is variable due to the payment methodology. The total income is guaranteed as a Present value in UFs. This means that each year the end date of a new concession is calculated.

For detailed information, please refer to “Roads Regulation” located in the valuation kit.